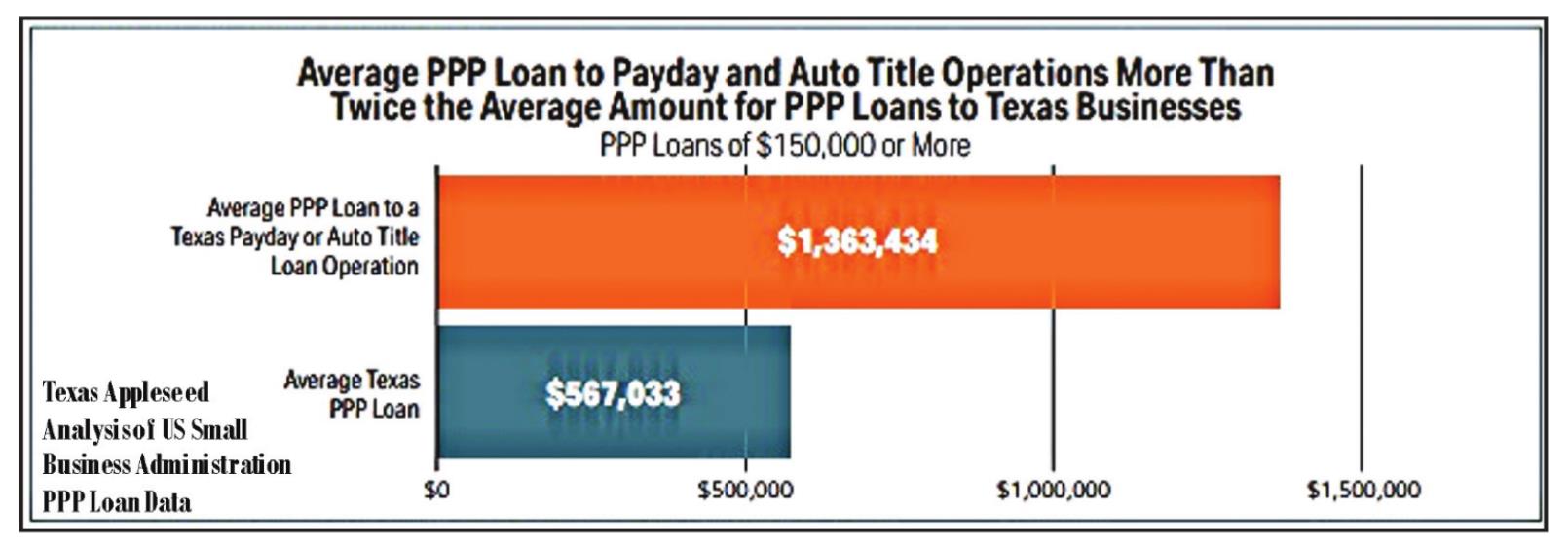

Paycheck Protection Program (PPP) funds are part of a federal program created through the CARES Act to help small businesses stay afloat and keep their workforce employed during the devastating COVID-19 pandemic.

A variety of small businesses qualify for these important funds, such as florists and hair salons, restaurants and cafes, family-owned contractors, and more. Many of these bu...